Let’s look at a range of approaches to satisfy (at least partially) the safety instinct of the ‘impalas’ and to temper the gung-ho instinct of the ‘lemmings’.

Staying ahead of Murphy’s Law

Often in business (and sometimes in life), it’s not one thing going wrong that will send you under, it’s everything going wrong at the same time. We’ve all heard stories about the guy whose luck ran out: he had a minor car accident, then found out he wasn’t insured; at the same time, one of his creditors didn’t pay on time and his business had cashflow problems that drove him broke; his wife left him, so he lost his house – and so on. It needn’t be a domino effect, where one thing leads to another: sometimes, things just happen all at once. Sometimes, everything can be going along fine – but it only takes a straw to break the camel’s back...

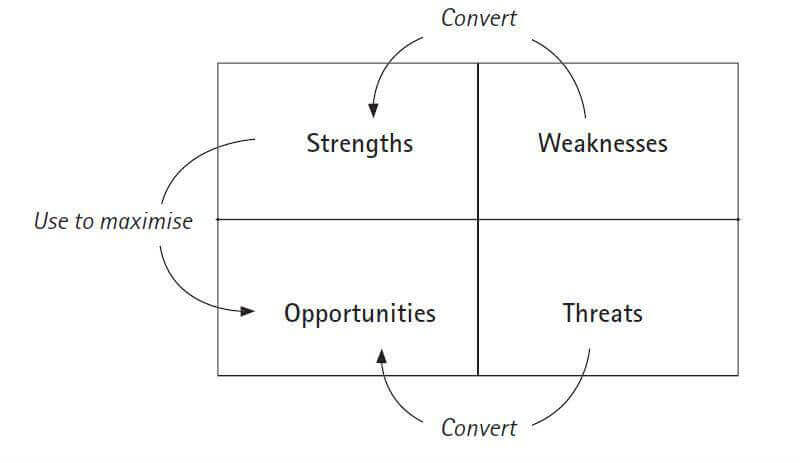

The point is, it helps to know when your camel’s starting to look creaky – and to see the straw coming! In my business I perform a SWOT analysis every six months – and I’m recommending that you do the same. SWOT stands for ‘Strengths, Weaknesses, Opportunities and Threats’. Strengths and weaknesses are internal aspects of your business (or success plan) that enhance or limit your ability to succeed and to cope with risk and challenge. I look at strengths and weaknesses in my character and personal skill set (as with the various ‘profile’ assessments in this programme); in my relationships; and in various aspects of my business (values, staffing, capital, structure and systems, client base, communication and so on).

• What do we do well, or better than competitors? What prevents us from doing as well as we could?

• What things enable us to capitalise on opportunities as they arise? What things limit us?

• What things enable us to cope with threats as they arise? What things hamper us?

Opportunities and threats are external aspects that may emerge to impact on your business (or success plan). Opportunities might be: a contact that might lead to profitable new contacts; newly-emerging demand for your talents, ideas or services; an asset or idea which currently appears to be undervalued by the market; or a new technology that will support your activities. Threats might be: a forthcoming rise in interest or tax rates; an emerging skill shortage that will make it more difficult for you to find staff; a direct competitor entering your market or ‘gazumping’ your ideas; changes in your own circumstances that will give you less time for your success plans...

• How might we capitalise on our strengths to create new success avenues? How might our weaknesses catch up with us and close success doors?

• What changes in our environment look like presenting us with new resources, ideas or opportunities? What changes threaten to limit, divert or break down our success plans?

• What are we excited and optimistic about? What are we afraid of?

SWOT analysis needs to be done every six months, because we are (we hope) constantly developing new strengths; weaknesses may emerge in response to different demands; and opportunities and threats are constantly coming into view. It's also important to do a SWOT review of each new team or partnership we put together to pursue our success: out combined SWOTs will be different from our individual ones.

Murphy's Law says that everything that can go wrong, will go wrong (eventually – and possibly all at once). Regular SWOT reviews enable us to identify the things that could go wrong (where our internal weaknesses might prevent us from meeting external threats) – so that we can plan accordingly.

As an example – and being brutally honest, here – the following grids represent my personal and corporate (Custodian Wealth Builders) SWOT reviews for last year.

John Fitzgerald Custodian Wealth Builders

Strengths

• Communication

• Relationships

• Determination

• Integrity

• Focus

• Leadership skills

• Big picture vision

• Strategy

Weaknesses

• Attention to detail

• Investigating alternative options

• Intolerance of non-task-related people

• Impatience

Opportunities

• Success coaching

• Mentoring

• Available finance

• Contacts

• Own personal development

Threats

• Lack of time

• Less land availability

• Family changes/health

Custodian Wealth Builders

Strengths

• Integrity

• Trust

• Unique brand

• Performance results

• Client base

• Referrals

• Product quality

• Price

Weaknesses

• Communication

• Supply on time

• Focus on John

• Lead generation

• Performance accountability

• Promotion

Opportunities

• New markets

• New products

• Direct/web marketing

• Market up-cycle

Threats

• Legislation/regulation

• Competitors

• Market down-cycle

• Bad press for industry

• Build on your strengths – in order to capitalise on the identified opportunities.

• Minimise your weaknesses – by working on those areas, or by recruiting people who have strengths in the areas of your weakness to your success team.

• Convert threats into opportunities – by developing strengths to counter them, and by being prepared to learn from them.

One further piece of advice on this (particularly if you’re a recovering ‘negative’ type): it’s more energising and efficient to focus on building on your strengths than on correcting your weaknesses. It’s about leverage: where can you use the smallest amount of time and effort to make the biggest difference and gain the biggest returns?

Think about people who have the perfect physique to be tennis players, but aren’t good at team sports. I’m told that if they work really hard, they may improve their tennis by 800%! If they devote the same amount of time to football, they will certainly improve – but they will never play football as well as they could have played tennis...

I’m good at big picture planning and strategy, and bad at detail. I could spend time learning to pay attention to the small stuff – and I’d certainly become a more rounded performer – but I would never make the kind of positive contribution I can achieve by devoting the time to fi ne-tuning my intuition and strategy. If I need attention to detail to maximise my opportunities, or minimise my threats, I can get someone on my team for whom that is their core strength.

Risky business

Your chosen field of success will have its own areas of key risk. If you’re a sports person or a dancer, say, the risk of physical injury or breakdown may be uppermost in your plans. But in most business projects, I think the key risks boil down to two areas: the people and the project.

People risks

People are your key resource in a business project – so they are also a key risk area. The wrong people, or loss of important people, can wipe you out. I remember a story told to me when I first started out in real estate: another one of those helpful fables...

The fable of the frog and the scorpion

Once upon a time there was a scorpion, who wanted to get from one side of the creek to the other. Being unable to swim, he asked a passing frog if he could catch a ride on his back. ‘But...’, said the frog. ‘How can I be sure you won’t sting me?’ ‘Why on earth would I do that?’ objected the scorpion. ‘I can’t swim. You might die – but I’d drown!’

This seemed sensible to the frog and he agreed to carry the scorpion across the creek. Half way across, swimming steadily, the frog felt a sharp pain in his back. ‘What have you done?’, he cried, as his legs grew weak and he began to sink. ‘You’ve killed yourself as well as me! ‘ ‘I couldn’t help it,’ said the scorpion, as he went under. ‘I’m a scorpion.’

There are people in business who will sting you – complicate things, cause conflict, look for problems, cheat you – regardless of the effect on their own reputation, effectiveness and prosperity. Perhaps, like the scorpion, it’s just their nature: either way, you can’t change them. But you can see them coming.

Then there are ‘sand castle’ people: people who build their sand castles really close to the water’s edge and love it when the wave comes in and wipes them out... How do you pick the scorpion and the sandcastle person? Look at their track record. If you want to do business with somebody, you’ve really got to know what projects they have previously done; what motivated them to undertake those projects and whether they succeeded (or didn’t succeed, but acted with integrity, and learned from the experience). You’ve got to know whom they have done business with in the past, and how those relationships (with partners or consultants) worked out.

Ask those few tough questions – and don’t take the answers at face value: arrange to talk to the past partners and look at the past projects. (If your prospective partner takes offence or puts barriers in the way of this legitimate investigation, warning lights may go on...) You’re looking for signs that a person has motivation to do the right thing well, and to see it through to completion. You are looking for signs that a person conducts business relationships with integrity and flexibility. If you get a glimpse of conflict, pending or past litigation, partnerships where ‘everybody else’ did the wrong thing, or great projects that collapsed for lack of resource, planning or perseverance... don’t give this person a ride across the creek – and don’t contract to build sandcastles with them!

You have to assess this risk unemotionally. Scorpions and sandcastle people are great fun. They’re very persuasive. They can be the nicest people. They will tell you that they’ll look after you; they’ve learned from their past mistakes; they thrive on risk and adventure... But it’s simply too risky for you to do business with them. Let them prove themselves on a couple of projects before you have anything to do with them.

However good the credentials and track record of the people you enter into partnership with, as with any business project, it’s good to have an exit strategy – and to have your exit planned, going in... It’s not negative or ‘untrusting’ to go into a partnership with a clear idea of how it can be unravelled. The point is to be able to unravel it in the simplest and most positive way for both parties (ideally without involving a third party who has an interest in dragging out any potential conflict: for example, lawyers!).

I’ve often backed out of joint venture agreements, because we couldn’t agree on a clean way to unravel the partnership if things went bad. I can assure you that you don’t want to be tied to partners who don’t want to be in the project, or who have lost heart for the project: they can make life unbelievably unpleasant. There has to be a clear trigger for unravelling the partnership: some objective marker which tells both of you that you have got as far as you are going to get together. And there has to be a clear process for unravelling the partnership.

Discussing this up front, before you sign into a partnership, may feel a bit like proposing marriage to someone – and immediately negotiating how you would go about getting a divorce. (That’s exactly what ‘pre-nuptial agreements’ are for.) You’re not ‘jinxing’ the partnership, or stating that you don’t think it will last: it’s just sensible risk management. If your prospective partners are scorpions or sandcastle people, it will weed them out – or enable you to protect yourself when their different agendas emerge. If they are people of good intent and motivation, it will be an opportunity to put all cards on the table – then forget about them, in fruitful collaboration, until (or if) the worst happens.

Have the discussion. Include in your partnership agreement terms which state exactly how, at the election of either party, you can part ways: what notice periods are required, whether one partner can buy the other out, how assets will be divided up, who will value them and so on.

Project risks

Obviously, every particular project and environment will have its own distinctive areas of risk. Most business ventures, however, will have:

• Demand-side risks: i.e. the risk that not enough people will buy your offering/product/service at a price that will give you the profit you need. As with people risks, you need an exit strategy. In commercial terms, this means that you need to make sure as far as possible in advance that you have a market which will be willing to pay a profitable price for your offering. In my field of property development, most financing organisations are going to want pre-sales (a percentage of the building sold off the plan) before they commit to funding. Whatever you’re planning to develop or sell, it’s a good idea to go out and canvas some potential buyers. Would they buy this particular product or service? How much would they pay for it? If you pre-committed to delivering this particular product or service at that price, would they pre-commit to buying it?

This not only gives you a head start on sales: it’s an essential part of marketing. It enables you to gauge what the market wants: how much your potential customers are prepared to pay, what features they want and value in the product or service, who/what they think your competitors are, and so on.

• Supply-side risks: i.e. the risk that you will not be able to provide the product/service as specified, at the specified price and time, and do it repeatedly in response to demand.

You might be surprised to learn that most builders and developers go bust in booms – not downturns. Why? Because they commit to pre-sales at a certain price, and then find that they can’t do it on time and on budget – and end up selling a building for less than it cost to build... Wherever possible, try and control or lock-in the key factors in your ability to supply your product/service as promised: whether they be cost or time or quality. When my company produces our educational products, we (naturally) get competitive quotes for printing and assembly of our folders, CDs and so on: it’s amazing how the unit cost varies, depending on where you get the work done and how many units you order. You can get unit costs down by ordering higher quantities – but that’s false economy. I always aim for a small initial production run, which I can use in a market test: a test run, evaluating the supplier’s quality, delivery, co-ordination and reliability – and (if necessary) refining the product in response to market feedback. I don’t want large stocks of a product that nobody quite likes. And I don’t want to be making quality or delivery promises to customers (based on suppliers’ promises to me) which we turn out not to be able to fulfil. I’d rather pay double or even triple the unit cost of 10,000 units, to get 1,000 units at a lower overall cost, which is invested in this market test. It’s like a racing car that comes in every few laps for a pit stop. They don’t make major changes: they just do a little tweaking here and there and send the car back out again; tweak and send back out... Remember the Japanese concept of kaizen: a process of continuous small improvements...

• Finance risks: Some non-financially-minded people are put off by the term ‘budget’, but budgets are simply plans with money values put to things. You’ll need a budget for where you will get the money to fund your plans: a capital budget. And you’ll need a budget for weekly or monthly cash incoming and outgoing – to make sure that you can meet your commitments at any given time: a cash flow budget. (Cash is like oxygen: if you run out of it, everything goes dark pretty quickly...) I’m not going to teach you about budgeting: I recommend that you get a good accountant onto your support team. But it’s important to realise that if your success plans depend on finance, you will have to build finance into your success plans! Give some thought to (or talk to your accountant about) financial risk management. Think through worst case scenarios. Budget for unexpected expenses, delays and cost rises. Take out relevant insurances.

Summary: insurance strategies

The following is just a checklist of some of the ‘insurance’ strategies you might use for risk assessment and management. The aim is still to leap – but to do so responsibly.

Assess the risks: get the information and advice you need to get a realistic idea of costs, pitfalls, common errors and downsides before you go in. If possible, talk to someone who’s been there, done that and made the mistakes! (Learning from your mistakes is good: learning from someone else’s is even better…)

Carry out regular SWOT analysis to identify risks in yourself – and in your environment – as they emerge. Use it to build on your strengths, capitalize on your opportunities, minimise your weaknesses and prepare contingency plans for the threats.

Do your homework at every stage of your plans. Education and investigation are key tools of risk management. You need to know what you are doing.

Choose your partners and advisers wisely. Don’t be embarrassed to ask for proof of trustworthiness and knowledge/expertise before accepting someone’s advice or help! Choosing a member of your success team is no less important than selecting someone for a job – and should be considered in the same light. Gathering people who can complement your strengths and minimise your weaknesses is good risk management – but only if they are the right people.

Pace your goals: set short-term, staged goals with limited downside risks to each – rather than putting all your eggs in one basket up front. This way, you can pull out, or adjust the plan, at each stage, without having lost too much time or resource. And you reduce the risk of biting off more than you can chew. (You still have to move outside your comfort zone, though…)

Plan your exit strategy before you go in. How will the asset be sold on – and to whom? What can be set up (or even guaranteed by contract) in advance? How will the partnership be terminated, if and when required? You are quite entitled to stack the cards in your favour, so that – if anything is happening that you don’t like the look of, you can simply walk away. If a high-risk deal, opportunity or partnership won’t give you that kind of protection – give it a miss: there will be another, more manageable one around the corner.

Have a fall-back position. Make contingency plans to deal with foreseeable problems and eventualities. ‘If x happens, I will minimise the impact/cost by ….’; ‘If I can’t get agreement on my preferred option, I will be prepared to accept…’

Take out insurances. You can find cover for most of the potential (financial) risks you might foresee – and insurers are often good people to help you identify risks you would never have thought of on your own! (Even if you don’t buy the policy, a useful discussion to have…)

Mix high- and low-risk strategies. In my wealth-building programmes, for example, I cover both ‘passive’ (low-risk, moderate-return) strategies and ‘accelerated’ (high-risk, high-return) strategies – and this is reflected in my own investment portfolio. Spread and limit your exposure, so that you’ve always got a relatively secure fall-back somewhere. (This doesn’t only apply to financial risks, either. We need to mix the new with the familiar, challenge and support, in order not to stretch ourselves too far…)

And then LEAP!

>>> Coming Next: Energiser Strategies

Please note: This is an extract from the Success From Scratch – it may not contain the exercises from the full version of the book/audio set, for full version please contact us or follow our blog for more.

Thank you,

The team@Custodian